Insurance for Engineers, Part 1

Why a $7T industry has no efficiency conversation

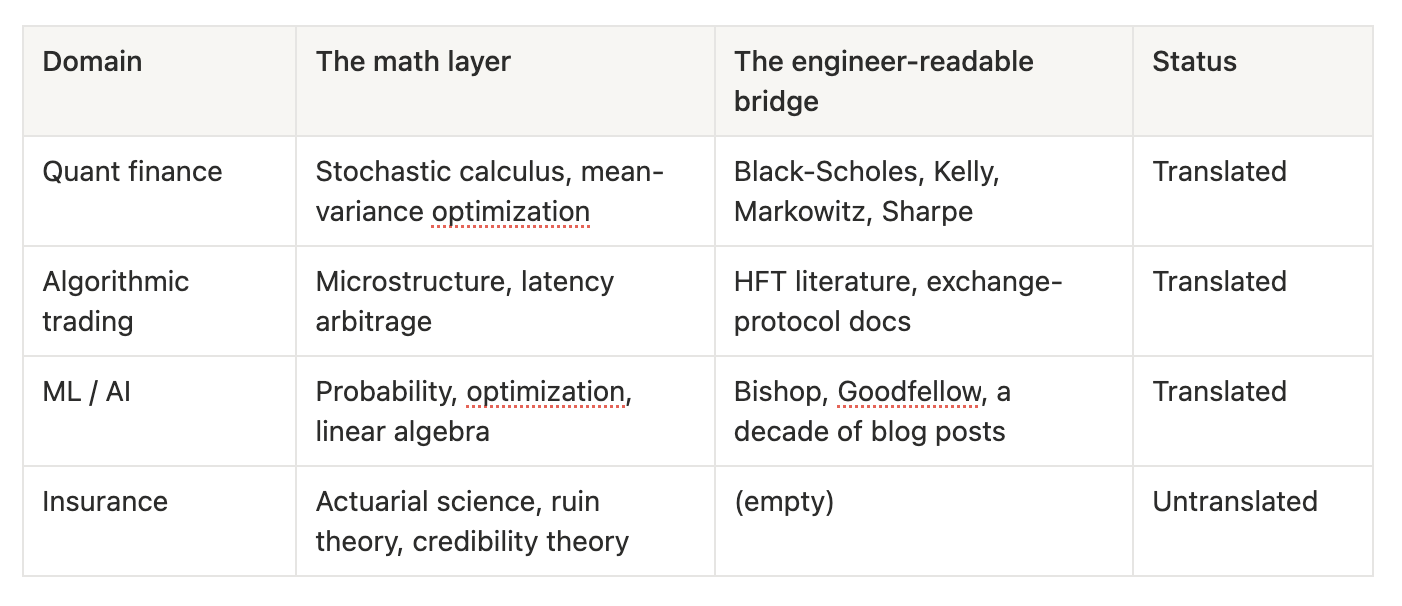

The translation gap

An engineer can read a Two Sigma whitepaper, argue about Kelly sizing over dinner, and explain why high-frequency trading competes on nanoseconds. That same engineer will bounce off an insurance company’s annual report in ninety seconds.

That is strange, because insurance is closer to a factory than to a fund.

Quant finance got translated for engineers. Markowitz gave us portfolio theory, Black and Scholes gave us option pricing, Kelly gave us bet sizing, and Shannon’s information theory found its way into betting markets. Three bridges that got built across thirty years. By the 1990s an engineer could open Active Portfolio Management and recognise half the math to be from a control-systems textbook.

Insurance never got that bridge. The actuarial math today is rigorous and largely settled. But the operational system wrapped around the math has never been written down in engineering language. So an engineer sees “loss ratio” and assumes it is exotic.

It is not exotic. It is yield on a production line.

This series aims to build the missing bridge. Today we cover the lay of the land.

That empty cell that’s “untranslated” is the gap, and it has a price to it that millions of policy owners are already paying.

Capital and talent pour into fintech and only trickle into insurtech, not because the underlying math is harder, but because nobody made the system legible to the people who build systems. Translate a domain and you lower the activation energy for every smart outsider who might otherwise have walked past it. That is what this series is for.

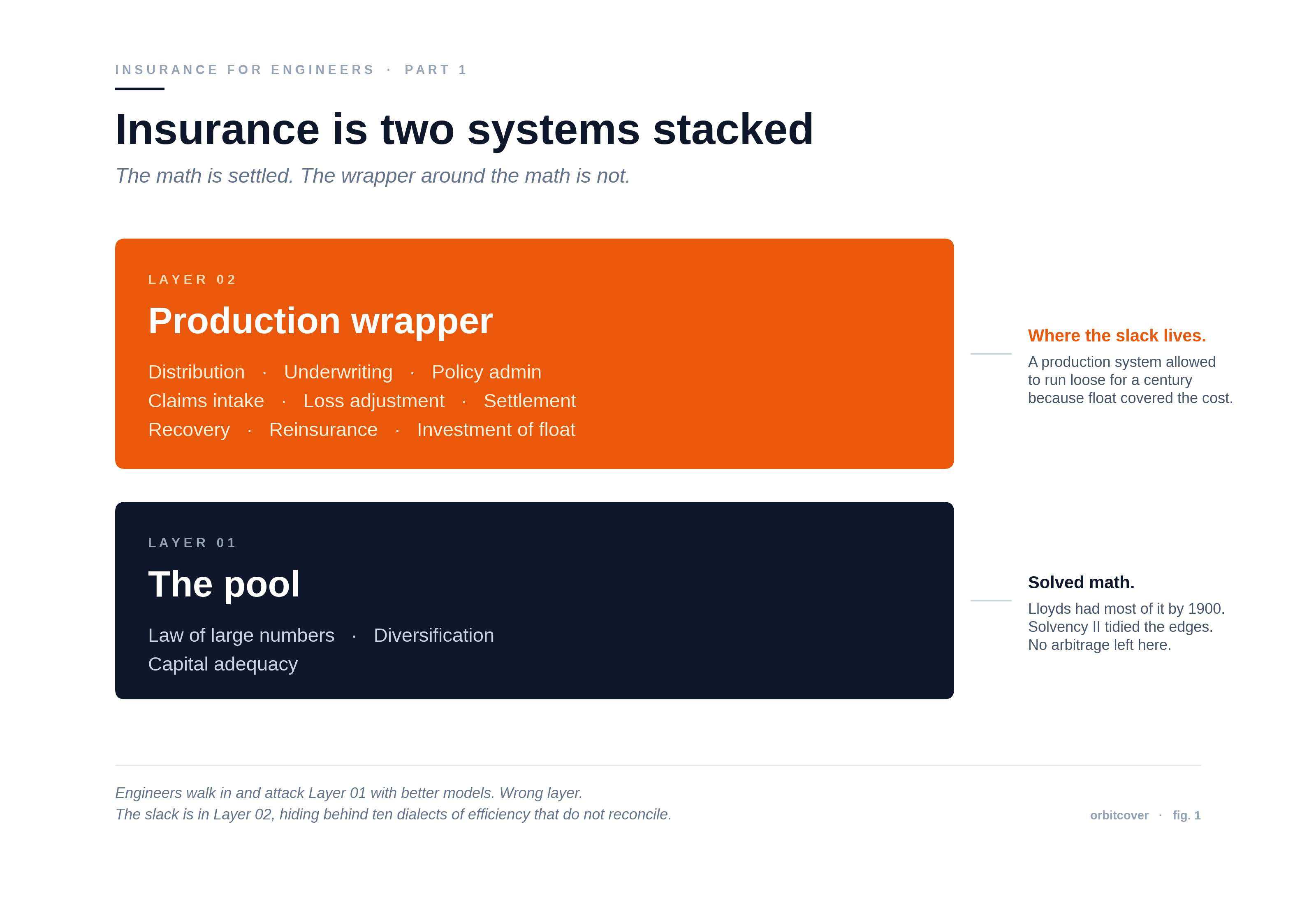

Insurance is 2-systems stacked one each other

The single most useful thing to tell an engineer about insurance is that it is two systems, not one.

Layer 1 is the pool: This layer is pure math: law of large numbers, diversification, capital adequacy. Long settled science that works like a well-oiled machine. Lloyd’s worked out most of it by 1900, and Solvency II tidied the edges in 2016. There is no innovation arbitrage left inside the pool itself today. Pricing a pool better is a game of basis points, played by people with PhDs, and the returns to cleverness there are thin.

Layer 2 is the production wrapper around the pool: distribution, underwriting, policy admin, claims intake, loss adjustment, settlement, recovery, reinsurance placement, and investment of the float. This is a production system. It runs on humans, paper, and workflows, and it is structurally slack.

Engineers walk in and attack Layer 1 with better models. That is the wrong layer. The pool math is doing fine. The slack lives in the wrapper. Trillions in premium flow through that wrapper every year, and almost none of it has been instrumented the way a factory floor is instrumented.

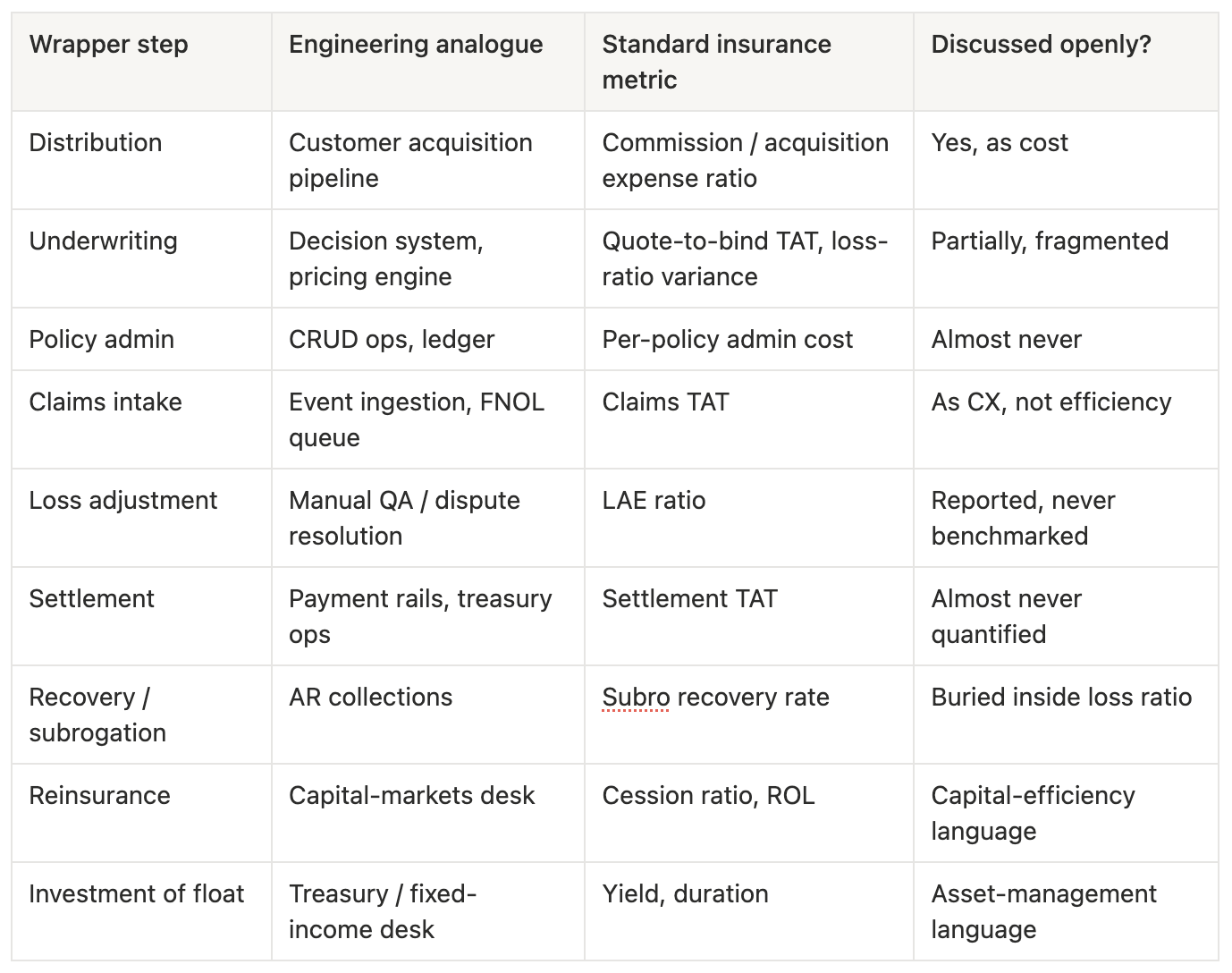

The production wrapper, mapped to engineering

Every step of the wrapper has an engineering analogue. Insurers do not use these names because they grew up speaking actuarial and regulatory semantics. Here is the dictionary.

Every row has an efficiency story. None of them roll up into a single integrated "production efficiency" view.

That is the actual answer to "where is insurance's efficiency conversation?" - It exists, dispersed across ten dialects that do not reconcile to one P&L.

Five reasons that no incumbent today says the word “efficiency”

Float economics: For a century, insurer profit came from investing premium reserves, not from underwriting margin. The conversation got captured by asset-management language: yield, duration, asset-liability matching. When the money is made on the float, operational efficiency is a rounding error, and it quietly stopped mattering. A carrier could run a 99 combined ratio for years and still print money on investment income.

Information economics: Akerlof, Rothschild and Stiglitz, Holmström. The intellectual frame of insurance is adverse selection and moral hazard. The canon is about information asymmetry, who knows what about the risk, not about throughput. Production language never got airtime in the textbooks, so it never got airtime in the boardroom.

Capital language took the word: Solvency II, IRDAI capital adequacy, US risk-based capital. When an insurance executive says “capital efficient,” they mean return on equity per unit of required regulatory capital. That is balance-sheet leverage, not operations. The most natural word for the thing we care about was claimed before operations could use it.

Balkanized metrics: Combined ratio, ROE, LAE ratio, persistency, expense ratio, attritional versus catastrophe. Each lives in its own silo and its own report. No insurer publishes an integrated production-efficiency dashboard the way a manufacturer publishes overall equipment effectiveness. There is no single number whose job is to go up when the line runs better.

The “we’re not factories” reflex: Operators see insurance as risk pooling, which is true at Layer 1 and false at Layer 2. The reflex is comforting, and it protects the wrapper from ever being optimized. Calling your business a craft is a good way to avoid measuring it like a factory.

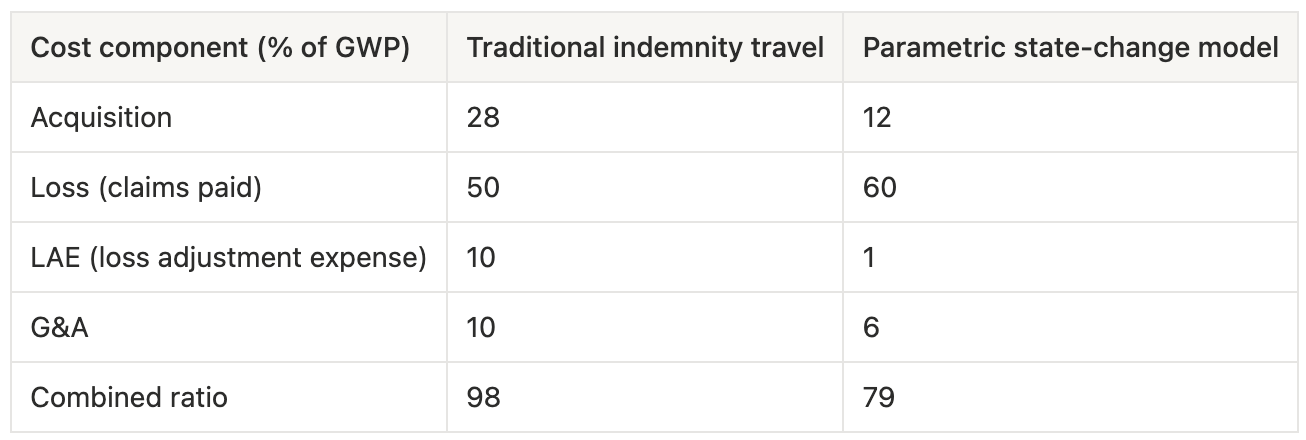

The cost stack, where the slack actually lives

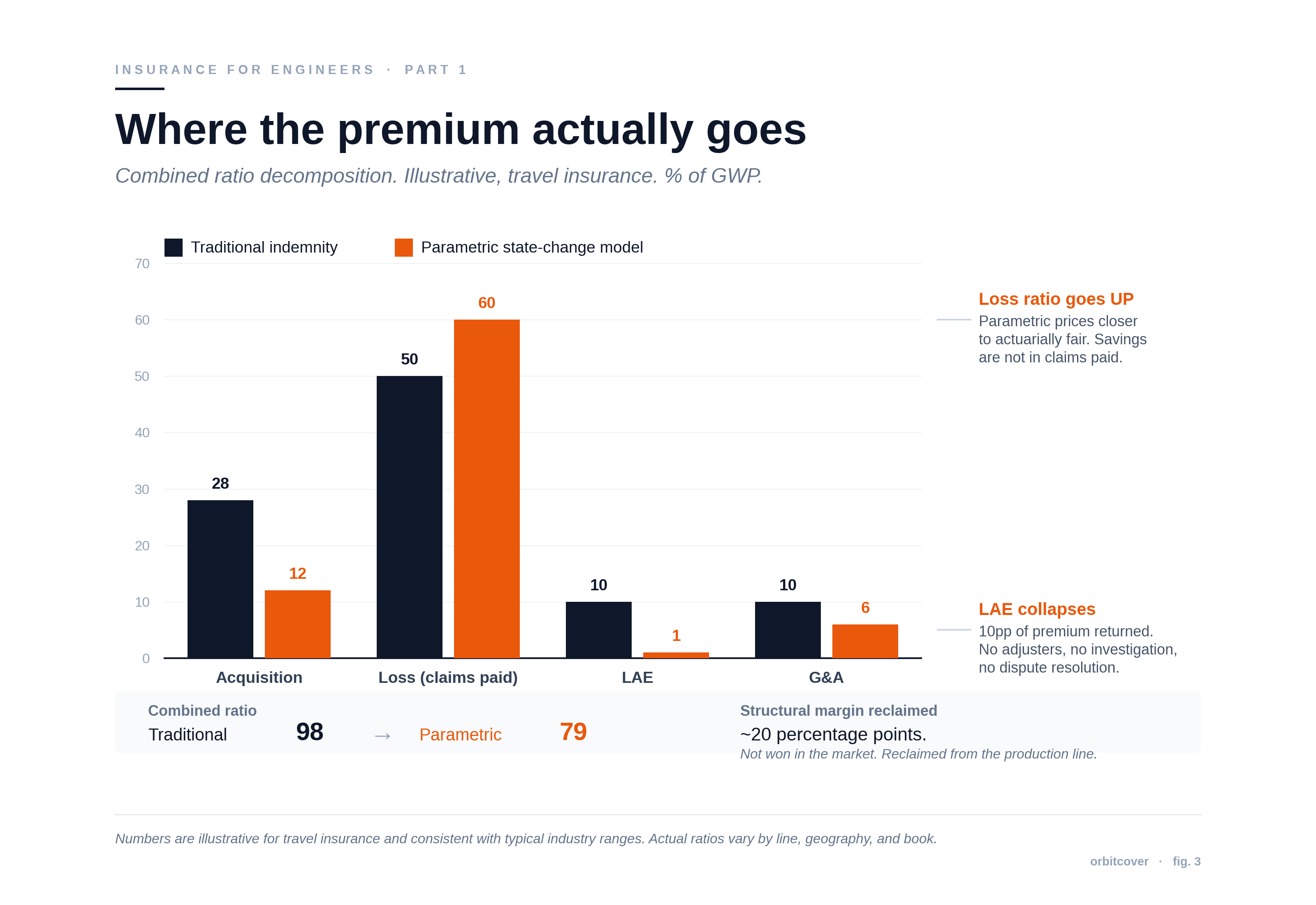

Decompose the combined ratio of a traditional indemnity travel product against a parametric, state-change model. Numbers below are illustrative and directional; treat them as the shape of the argument, not as audited figures.

Two non-obvious points sit under this chart.

First, the loss ratio goes up under parametric, not down. The efficiency thesis is not “we pay fewer claims.” Parametric pays more claims as a share of premium, because pricing sits closer to actuarially fair and there is no adjuster looking for reasons to deny. Every bit of the saving comes from somewhere else: the LAE line collapses from ten points to one, acquisition compresses, and G&A thins out. The customer gets paid more often and faster, and the economics still improve. That combination is the entire point.

Second, the combined ratio compresses by roughly twenty points structurally. That margin is not won in the market through pricing wars or clever distribution. It is reclaimed from the production line.

This is the moment a builder leans forward: twenty points of structural margin, sitting inside a wrapper that nobody is allowed to touch.

All the savings come from production-layer overhead.

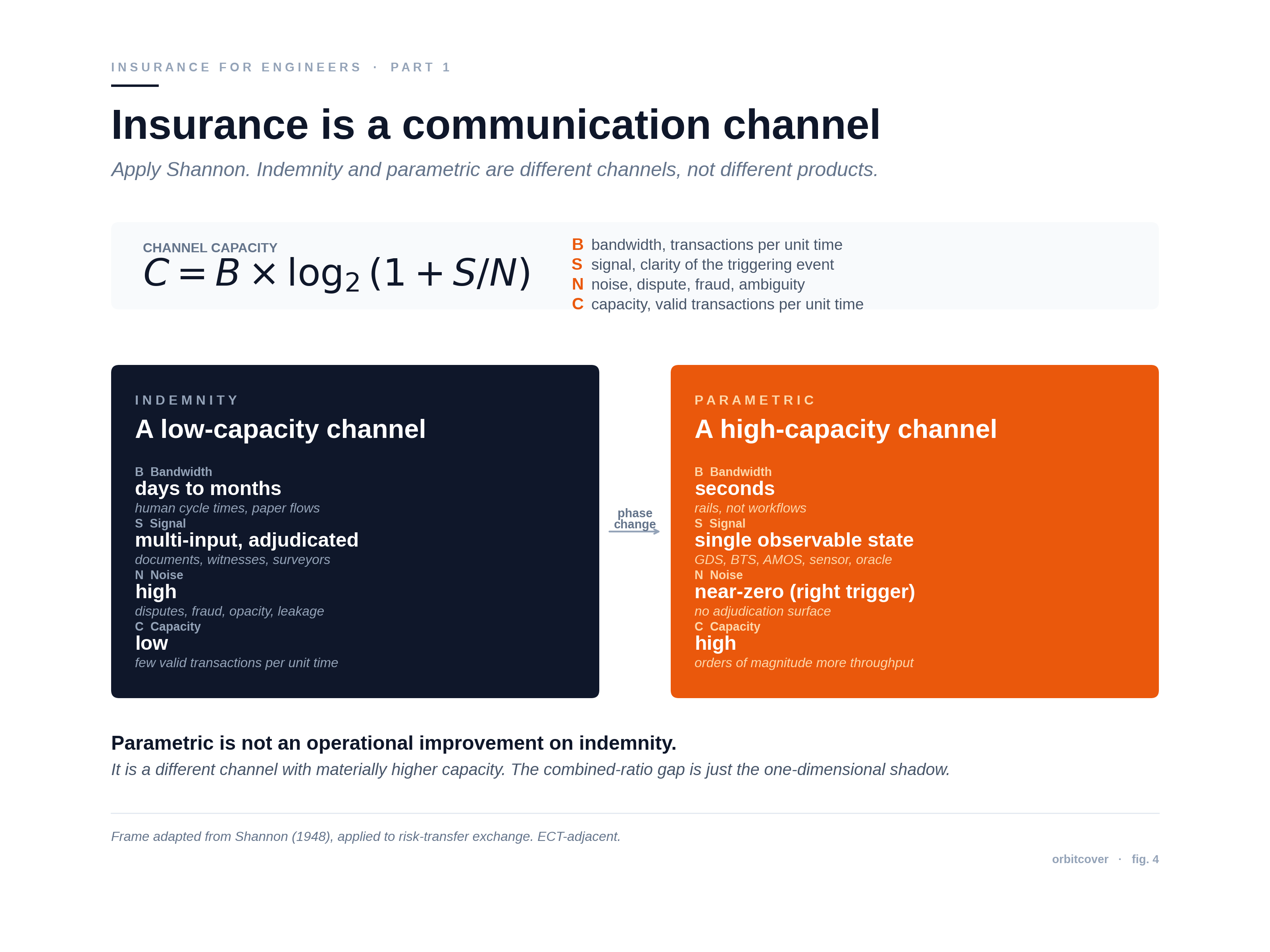

Insurance as a Shannon channel

Here is the frame that does not exist anywhere else in the insurance literature, and the reason none of the incumbent metrics capture what parametric is doing.

Treat insurance as a communication channel. The customer transmits a state (”I had a loss”). The insurer transmits a state back (”here is your payout”). Shannon already wrote the equation that governs this kind of system:

C = B × log₂(1 + S/N)

B = bandwidth, transactions per unit time

S = signal, clarity of the triggering event

N = noise, dispute, ambiguity, fraud, investigation overhead

C = channel capacity, valid transactions per unit time

Indemnity insurance is a low-bandwidth, low-S/N channel. Settlement takes days to months, so B is small. The signal is noisy, because deciding whether a loss happened and how much it cost needs human adjudication. Both terms are small, so capacity is small.

Whereas parametric insurance is a high-bandwidth, high-S/N channel. Settlement lands in seconds. The signal is clean, because the trigger is an observable state change in an authoritative system: a flight status, a weather index, a GPU SLA breach.

A traveller buys cover against a delayed flight. In the indemnity world, a delay means a claim form, a boarding pass, maybe a receipt for the airport meal, a queue, an adjuster, and a payout that arrives two weeks later if it arrives at all. Every one of those steps is noise in the channel: a place where the signal can be disputed, padded, or lost. In the parametric world, the trigger is the flight’s own status feed. The aircraft lands 03:14 late, the threshold is two hours, the contract reads the same authoritative record the airline reads, and the payout is pushed to the traveller’s card before they reach baggage claim. Same insured event. A different channel.

Both B and S/N jump by orders of magnitude. Parametric is a different channel with materially higher capacity. The combined-ratio gap from the previous section is a one-dimensional projection of a multi-dimensional capacity jump. (This frame is original, drawn from my ECT work in progress, so read it as a hypothesis worth pressure-testing, not as industry consensus.)

Parametric is not a marginal operational improvement. It is a different channel.

What this means for builders and capital

The slack is structural and reclaimable. Roughly twenty points of combined-ratio compression sit inside the production wrapper of a $7T global industry. That is not a marketing claim. It is what falls out when you strip LAE, compress G&A, and remove the recovery cycle. Insurance ran loose for a century because float income covered the looseness, and the slack accumulated where nobody was looking.

Incumbents will not take this efficiency voluntarily. A faster settlement cycle is a worse business for a carrier optimizing on float income; money that pays out in seconds cannot be invested for months. That single fact is the most important structural truth in the space, and it is why the margin is reclaimable by a new entrant rather than competed away by the incumbents who could, in theory, copy it. The people best positioned to build this are the people with the least incentive to.

Trigger selection is the whole game. Parametric trades operational risk for basis risk: the risk that the trigger fires when no loss occurred, or fails to fire when one did. Basis risk is bounded only when the trigger correlates tightly with the insured event. Flight delay to delay payout is a correlation near 1.0. Drought index to actual crop loss is a correlation of 0.5 to 0.7, which is exactly why parametric crop insurance scarred a generation of farmers who watched their fields die while the index said they were fine. AI-native parametric is the natural form here, because trigger design, oracle integrity, and dynamic pricing on observable state are precisely the problems modern compute is built to solve.

I am building OrbitCover on a single bet: that an AI-native parametric insurer can hold the full reclaimed margin while staying honest about basis risk. The rest of this series works through how.

Coming in this series

The parametric stack, in detail. State-change pricing, oracles, settlement rails.

Why “AI-native” means event-driven and deterministic, not generative.

Basis risk, honestly. When parametric works, when it fails, and how to tell the difference.

Reinsurance as bandwidth. Why capital structure is the real moat.

ECT, formally. Insurance, exchange, and Shannon’s channel applied to risk transfer.