IUMI just published the case against its own architecture

Marine insurance's global trade body spent 39 pages documenting why claims-based models are losing. They didn't frame it that way. I will.

I was in Bengaluru at 1am on a Tuesday, three tabs deep into reinsurer outreach prep, when the IUMI EYE Issue 52 PDF landed. IUMI is the International Union of Marine Insurance. Their quarterly newsletter is written by and for the people who insure the world’s ships, cargo, and offshore energy infrastructure. Underwriters, surveyors, maritime lawyers, loss prevention specialists. These are the people who think about what happens when a container catches fire mid-Pacific or a tanker grounds off Turkey carrying soya beans.

I don’t insure ships. I build parametric insurance settlement rails. But the traditional insurance industry’s own publications are the best primary source for why parametric architecture needs to exist. And this issue delivered the data.

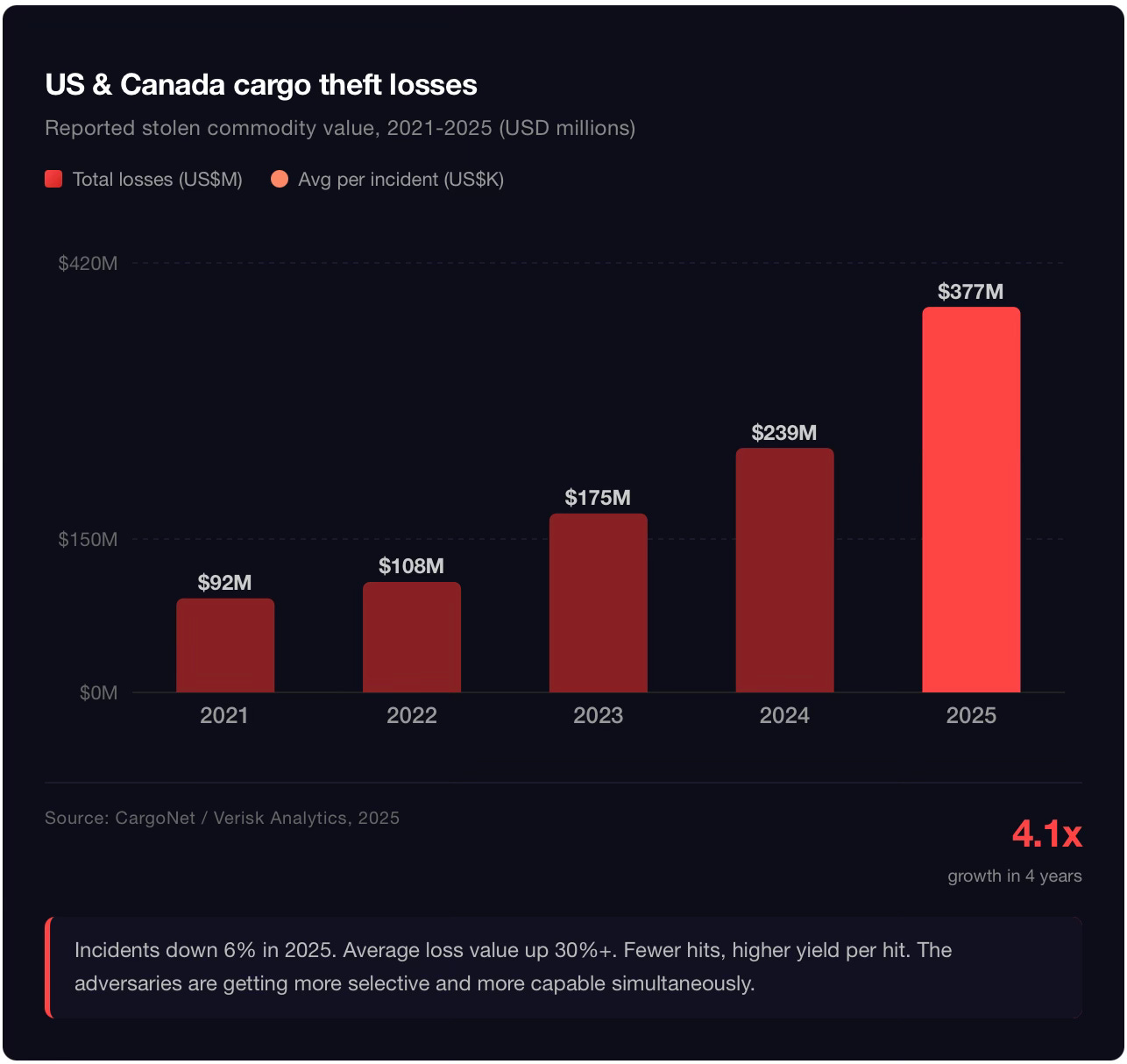

$92M to $377M in four years

The centrepiece is a special feature on “fake carriers.” IUMI and TAPA EMEA issued a joint warning: criminals are creating shell companies, cloning legitimate firms with stolen credentials, forging insurance certificates, and using generative AI to scale all of it.

The data behind the warning:

TAPA’s intelligence system recorded nearly 160,000 cargo-related crimes across 129 countries between 2022 and 2024. The total losses amount to billions of euros. In the US and Canada alone, estimated cargo theft losses hit $725 million in 2025. The average per-incident value rose over 30% year-on-year, even as total incidents dropped 6%.

Good news: Fewer hits.

Bad news: Higher yield per hit.

The adversaries are getting more selective and more capable at the same time. And this is something to worry about.

The industry’s response today? Continuous vetting of carriers and drivers. Deeper verification of contacts and documentation. Enable multi-factor authentication on freight exchange platforms. Implement more secure ID cards and scanners to read them. Cost, cost, cost and more cost.

Every single countermeasure proposed above is a human-verification step bolted onto an existing process. More checking of people. More scrutiny of people. More people examining more documents. Against unknown adversaries who are using genAI and/or LLMs to probably generate those documents.

The unsaid structural problem

The entire claims-based insurance model depends on documents being trustworthy. A “claim” requires a claimant to submit evidence. An adjuster evaluates that evidence. A decision is made. And then the money moves.

Every link in that chain is an attack surface. From the claimant’s identity, to the documentation, to the adjuster’s judgment, the communication channel; every layer is open to attack. Fake carriers exploit all four simultaneously.

This is what I call a need for the elimination thesis: parametric insurance doesn’t compress the claims adjudication process. It removes it.

When a payout is triggered by an external oracle (flight tracking data, weather stations, IoT sensors, port telemetry), there is no claim to file. No document to forge. No adjuster to deceive. No identity to spoof. The payout trigger is a fact about the world, not a narrative constructed by the claimant.

And every year that AI makes document forgery cheaper, the elimination thesis gets stronger. The fraud arms race is asymmetric in the wrong direction for traditional models, and symmetric in the right direction for parametric ones. Oracles don’t get easier to spoof as LLMs improve. Claims documents do.

2.79 out of 5

On Page 25 of the newsletter, there is an IUMI industry survey on digital transformation. The results are quietly devastating.

Only 31% of respondents use AI beyond internal experiments. Self-assessed digital maturity averages 2.79 on a five-point scale. The top barriers to AI adoption aren’t workforce resistance or training gaps. They’re legacy systems (22%) and data quality (26%). Core system modernisation doesn’t even top the priority list, despite being the prerequisite for everything else the industry projects and says it wants.

In the survey authors’ own words: technological ambition appears to be advancing faster than the underlying system architecture that would sustainably support it.

That sentence is the whole story. You can’t digitise a process whose fundamental architecture assumes and is fully reliant on paper-era trust models. You can only replace it.

64% of companies have dedicated internal digital teams, and 89% of those rely purely on internal capabilities. They’re trying to self-perform a paradigm shift. This almost never works. The railroad companies didn’t build the airlines. The postal services didn’t build email. The film studios didn’t build streaming.

The orphan function

There’s one more interesting data point in the report. When asked about digital priorities, over a third of insurers identified underwriting as their top focus. Claims transformation ranked well below.

If you think about it, this is exactly backwards from first principles. Underwriting determines premium income. Claims determines the payout. The technical result, the thing that actually decides profitability, is shaped more by claims than by underwriting.

But claims transformation is messy. It touches operations, legal, customer relationships, regulatory compliance across jurisdictions. Underwriting optimisation is comparatively clean: better data in, better pricing out. So the industry polishes the intake funnel and defers the structural problem to tomorrow.

The gap this creates is specific and exploitable. If you build settlement infrastructure that makes the claims function disappear for a defined product category, you’re solving the problem the industry has decided not to solve internally.

Signals from adjacent verticals

The rest of the newsletter is dense with expansion signals for anyone thinking in parametric terms.

Autonomous vessels. HGK Shipping got the first permit for a remotely controlled hazardous goods tanker in Flanders. German insurers say they’ll cover autonomous ships but demand full operational data access.

Their open questions (eg., who is legally navigating from a Shore Control Centre? how to allocate liability between shipowner and tech provider? how to establish causation in system failures?) are exactly the questions that oracle-based models answer by construction. The telemetry data IS the adjudication. There’s no “establishing causation” when the trigger is a sensor reading.

Supply chain disruption. The US-Israel Iran conflict has pushed container shipping surcharges to $3,000 per forty-foot unit. Maersk and CMA CGM suspended Red Sea routes. India and Pakistan are the most exposed to LNG disruption from the Gulf, and chaos is simmering with hyperlocal worries about shortages. Every supply chain shock creates demand for fast, automatic protection that doesn’t require a three-month claims process.

Port accumulation risk. A Latin American analyst applied Little’s Law (Inventory = Flow × Dwell Time) to port exposure. Colombian ports today hold $580-660M in cargo at baseline, rising to 2.25x under a 10-day disruption. That’s a clean parametric frame: if dwell time exceeds threshold X, payout triggers.

No loss adjuster walks through the port with a clipboard.

The conference theme tells us everything we need to know

IUMI’s annual conference in Rotterdam this September is titled “Anchoring Trust in a Contested World.”

The word “trust” is doing all the load-bearing work here. The system continues to depend on trust in the claimant’s identity, trust in documentation, trust in the adjuster’s judgment. The system’s own global trade body is publishing evidence that each of these trust layers is eroding fast, or becoming less dependable at current costs.

Parametric insurance doesn’t require trust in the claimant. It requires trust in the oracle. That’s a different engineering problem, and a solvable one.

The traditional insurance industry knows the current architecture is under stress. They document it meticulously, every quarter, in professionally typeset PDFs. They just can’t publish PR around the conclusion that follows from their own evidence.

So I will: the claims process, as an institution, has a shelf life. And the countdown is being accelerated by the very AI tools that the industry scores itself 2.79/5 at adopting.

I’m building OrbitCover, parametric insurance settlement infrastructure. We automate payouts using external data triggers and settle via UPI in under four minutes, zero human claims handling. If you’re thinking about what comes after claims, let’s talk.

The gap between what the industry measures and what it actually needs to fix is getting pretty clear